This month, I’d like to take another story from Statesmen of the Confederate Cause by Burton J. Hendrick to tell the tale of the $15,000,000 in Confederate bonds.

This month, I’d like to take another story from Statesmen of the Confederate Cause by Burton J. Hendrick to tell the tale of the $15,000,000 in Confederate bonds.

Having failed to gain English and French recognition in the first year of the American Civil War, the Confederate government found itself in possession of 450,000 bales of cotton which it had purchased and held in port in order to create cotton shortages in the mills of Lancashire and northern France, causing such economic turmoil that those nations would ally through necessity. Last month, we discussed why that did not come to pass.

Accordingly, as winter came to an end in 1862, the Jefferson government held possession of what should have been an extremely lucrative product if it could be moved to Europe. The increasing effectiveness of the Federal blockade did prevent its shipment overseas, particularly after April 1862 when Farragut captured New Orleans. Nevertheless, the cotton did present the potential for future wealth which proved too tempting for European speculators.

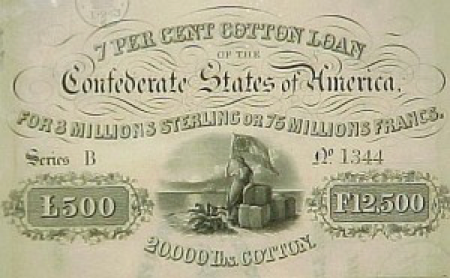

The banker who rose to the challenge was a certain Emile Erlanger, of Erlanger et Cie in Paris. Erlanger offered to raise $25,000,000 in gold in exchange for Confederate bonds guaranteed by the cotton bales then sitting in Confederate warehouses. The success of this arrangement depended of course on Confederate victory. In September 1862, this seemed the likely outcome following the Confederate victories of the previous summer and the predisposition of European elites towards an eventual dissolution of the United States, a country ruled as a democracy by rabble-rousing, venal politicians instead of a titled elite.

After negotiations in which Judah P. Benjamin, then Secretary of State, led the Confederate side, the resulting terms required the Confederate government to redeem the bonds at face value. The bonds could be purchased for gold at 77% of face value. They would carry 7% per annum interest until redeemed. Unlike the majority of loans to stable governments, the Erlanger loan demanded the Confederacy redeem these bonds at full value for Mississippi Valley cotton at the rate of twelve cents per pound not less than six months following the ratification of a treaty of peace between the United States and the Confederacy.

Such was the sense among European investors that, following the paucity of cotton for the duration of the American war, they would control the European cotton market and thus reap an eight-to-ten-fold bounty on their investment.

Erlanger had underwritten the entire loan at 77% of face value; however, when the bonds became available for sale on March 18, 1863, demands for subscriptions reached $80,000,000 in the first week of sale, although only $15,000,000 had been put on sale. Erlanger offered the bonds to the public at 90%, yielding an immediate profit for Erlanger et Cie of $1,950,000, not including sales commissions. The value of shares peaked shortly afterwards at 95.5%. Subscribers were required to pay 15% of their pledge upon initial sale and installments thereafter.

The furor continued into early April 1863. However, values began a period of downward fluctuations by mid-April. The causes for this downward trend have not been fully documented. Certainly, Federal successes in the Western theater, such as Union victories at Fort Donelson and Donelson, Nashville, Shiloh, and New Orleans had some effect, but that probably news of these victories was off-set by Lee’s victories in Virginia, the more widely-reported front.

A more plausible explanation is the efforts of the Federal ministers to France and England, Charles F. Adams and John Bigelow. Little documentation exists to identify specifically how the Federals worked to devalue the shares in the loan but what does exist implies that William Seward, Federal Secretary of State issued instructions not only to paint Jefferson Davis as a “Repudiator” who had defended the default on Mississippi’s state debt while a senator from that state; but also, to purchase as many shares as possible in the loan and then resell those shares at the lowest possible prices. Their counter-schemes worked so successfully that concerns arose within Erlanger et Cie that the investors would abandon their subscriptions altogether, even forfeiting sums already paid.

These fluctuations continued through the Spring and into Summer. Faced with the possibility of huge losses, Erlanger et Cie went to work. In order to shore up the value of the shares, the company embarked on a massive buying campaign. However, as bankers are want to do, their plan did not involve using their own resources. By employing coercive tactics on the Confederate representatives, they used the sums already deposited by investors in the Confederate loan to buy-back shares of the same loan. Ultimately they used about $6,000,000 in the buy-back campaign.

The fluctuations continued until the European public realized the impact of the trio of defeats at Gettysburg, Vicksburg, and Port Hudson in late July 1863. Thereafter, the value of shares plummeted.

Having squandered $6,000,000 of the Confederate government’s receipts, can you guess who were the greatest beneficiaries of the Confederate bond offering? Confederate Treasury obtained over $5,500,000 to purchase European arms, ammunition, medicines, and other military supplies and to outfit Confederate raiders. However, it was the bankers who saw the greatest returns. Not only did they collect $3,000,000 of the above amount from the Confederate government in the form of bankers’ commissions and other contract requirements, but the majority of the $6,000,000 used to buy-back shares went into the private accounts of the officers of Erlanger et Cie, since they were the first owners offered the opportunity to sell their shares back to the Confederate government!

We can see a number of interesting outcomes from the scandal of the Confederate Loan. First, the beneficiary of the loan, the Confederate government actually paid more in banking fees than they received from the bond issue. Second, the Confederate Minister to France, James Slidell developed a closer relationship to the Erlanger family. In October 1864, his daughter Mathilde married Frederick Emile Baron d’Erlanger, the very manager of Erlanger et Cie responsible for the Confederate bond issue.

Lastly, it is interesting to speculate about the post-war politics surrounding a Confederate victory won in part through bonds held by the Federal government. These held a commitment to deliver $15,000,000 (plus 7% interest) worth of New Orleans middling cotton, at twelve cents a pound, not less than six months following the ratification of the treaty of peace.

Sean Gabhann

The Seven Percent Solution